There has been acute interest in the inversions currently taking place on the term-spreads around the world:

And this comes as no surprise, since more than half of the world’s sovereign yield curves have now inverted…

Right now, 70% of the U.S yield-curve cluster comprising the 10/5/3/2/1 year bond yields are inverted as shown below. In prior research we have advocated using greater than the 60% threshold to have a “guaranteed lock-in” of the inversion:

A closer inspection shows that the 10-year less the 2-year is on the cusp of inverting, which will mean 80% of the yield curve complex will have inverted when this happens:

It is interesting to note that the current inversion process is very different from the past. In the past we have inflation and short rates rising as the economy overheated whereas now we are seeing both the long and short rates falling rapidly. The past trend of the last 7 inversions had the short term rates rising faster than the long term rates. This time around, the long term rates are collapsing faster than the short-term rates:

We do not think this changes any of the historical inversion connotations. The distortions and behaviors driven by short rates being higher than long rates still applies in our view. However, this difference in itself is more accommodating to the economy since rates are falling (as opposed to rising in the past). Even if the US economy falls into a recession, it’s likely to be less severe than recessions in the past.

There are a lot of theories on why a yield curve inversion causes a recession. This one is our favorite purely because of its simplicity:

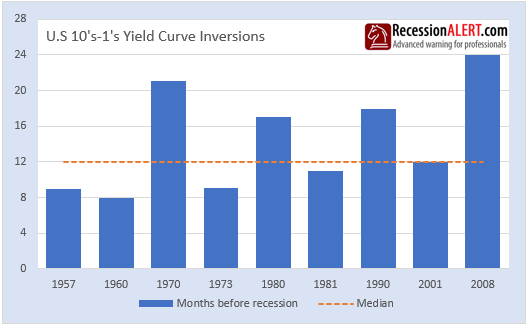

As we have stated before, there is not much use in knowing a recession is coming in 12-24 months time since the post-inversion stock market peaks and variances in the leads to recession are too widely dispersed (wide standard deviations) to be of practical use. However, for those that are curious, here are the leads to recession after a 10’s vs. 1’s yield curve inversion:

The two smallest lead-times to recession average 8 months, the median lead-time is 12 months and the two longest lead-times average 22 months. This puts forward the following dates for recession:

Comments are closed.