On 17 April 2026 Iran’s Foreign Minister Abbas Araghchi posted on X that the Strait of Hormuz was “completely open” to all commercial vessels for the remaining duration of the Lebanon ceasefire. The S&P 500 closed above 7,100 for the first time. The Dow rallied nine hundred points. Brent crude futures fell 10.7% to $88.73 in a single session. Nasdaq printed a fresh all-time high. The market treated the post as the end of the crisis.

The crisis is not over. Nothing that happened on 17 April repaired a compression train at Ras Laffan — the Qatari gas facility that liquefies approximately twenty percent of global LNG flows — refloated a shut-in field in Basra, cleared the eight hundred million barrels of crude sitting in loaded tankers anchored in the Gulf, or relaxed the United States naval blockade on Iranian ports, which Donald Trump, within hours of thanking Tehran on Truth Social, confirmed would remain “in full force” until a permanent deal including the nuclear programme is reached. The physical world did not move. The paper world did.

Donald Trump confirmed the United States naval blockade of Iranian ports would remain “in full force” until a permanent deal including the nuclear programme is reached — within hours of Araghchi’s post. The Lebanon ceasefire killed its first civilian in southern Lebanon within twenty-four hours of taking effect, with the Lebanese army formally reporting Israeli shelling of southern villages on day one. Neither condition that underpins the “completely open” declaration remained intact on the day it was made.

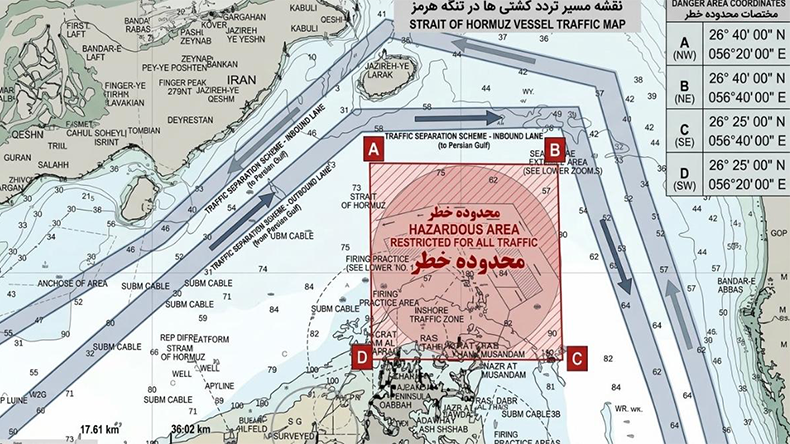

What Araghchi announced is not the pre-war Traffic Separation Scheme — the international shipping lane corridor established under the 1982 UN Convention on the Law of the Sea — reopening. It is a five-mile-wide permission corridor inside Iranian territorial waters, routed north of Larak Island inbound and south outbound, administered by the Islamic Revolutionary Guard Corps Navy, with pre-clearance required for every hull, a two-million-dollar transit toll codified into Iranian law on 31 March, discretionary nation-by-nation approval, and an expiry date — 26 April — tied to a Lebanon ceasefire that killed its first civilian within twenty-four hours. The toll is payable only in Chinese yuan routed through Kunlun Bank outside the SWIFT system, in Bitcoin, or in USDT. The IRGC is a United States Treasury Specially Designated National and a Foreign Terrorist Organization: every available payment method is a direct sanctions violation carrying civil penalties up to one million dollars per event, criminal penalties up to twenty years, and — per Trump’s explicit instruction the same week — interception by the US Navy of any vessel that has paid. Hapag-Lloyd, one of the world’s largest container lines, said on 17 April that “there are still some open questions” — insurance coverage, exact sea corridor orders from the Iranian government and military, and sailing sequence — and that until they are resolved, its vessels will not transit. Insurance cannot be procured because standard Protection & Indemnity club policies void on sanctions breach. Maersk has not moved. MSC has not moved.

Paper markets price narratives. Physical markets price molecules. On 17 April the narrative was resolution — the S&P 500 printed an all-time high, Brent futures fell 10.7%. The molecules had not moved. The IEA’s March supply record, the EIA’s April shut-in projection of 9.1 million barrels per day, and Lloyd’s transit count of 5.7 ships per day were all unchanged before and after the announcement. The divergence between what paper priced and what physical delivered has been widening since late February. The 17 April rally widened it further.

This is the recurring distinction that anchors the rest of this note, and that markets are refusing to price. On 17 April the narrative was resolution; the molecules, the tonnage, the refineries, and the LNG trains had not changed. The International Energy Agency recorded the largest oil supply disruption in its history in March — global supply fell 10.1 million barrels per day; export losses exceeded 13 million. The Energy Information Administration projected Middle East production shut-ins rising from 7.5 million barrels per day in March to 9.1 million in April. Neither agency has revised those figures downward. Neither agency can, because a corridor being declared open does not rebuild what has been physically destroyed, does not manufacture liquefied natural gas for which no pipeline alternative exists, and does not dissolve the legal pincer between Iran’s payment demands and United States sanctions law. The strait is a traffic signal. The crisis is a production, infrastructure, and legal-architecture crisis. Announcing one green does not fix any of the others.

Araghchi’s “completely open” corridor is not a shipping lane. It is five interlocking conditions, codified over the preceding seven weeks, that together mean no major Western shipping company can use it. Each condition is individually navigable. Stacked, they are a trap.

Corridor. Five nautical miles wide, north of Larak Island inbound and south outbound, entirely inside Iranian territorial waters. The pre-war Traffic Separation Scheme ran roughly twenty nautical miles wide through international waters under the 1982 UN Convention on the Law of the Sea; the IRGC corridor is one-quarter of that geometry. Every vessel transits under one-by-one Revolutionary Guard naval escort. At roughly one hour per hull including pre-clearance vetting, the physical throughput ceiling is twenty to twenty-four transits per day — against a pre-war norm of one hundred to one hundred and thirty-five. Lloyd’s List Intelligence logged 5.7 transits per day in March 2026. The corridor is a bottleneck by design, not a lane that can be scaled by announcement.

Toll. Two million United States dollars per vessel, codified into Iranian law on 31 March 2026 under the “Strait of Hormuz Management Plan” — the first toll imposed on an international waterway in more than a century and a half. Payment is accepted in Chinese yuan routed through Kunlun Bank on the Cross-Border Interbank Payment System — China’s dollar-alternative settlement rail known as CIPS — in Bitcoin, or in USDT. Kunlun has been sanctioned previously by OFAC for handling Iranian payments. The Islamic Revolutionary Guard Corps is simultaneously a Treasury Specially Designated National and a State Department Foreign Terrorist Organization. Every payment method is a direct US sanctions violation carrying civil penalties up to one million dollars per event and criminal penalties up to twenty years. At pre-war throughput, the toll would generate roughly two hundred and seventy-six million dollars per day — approximately one hundred billion dollars per year — denominated outside the dollar system and flowing to an FTO. This is revenue architecture, not a service charge.

Approval. The IRGC retains discretionary power over which nationalities transit and which cargoes. Bloomberg, Kennedys Law, and Bracewell LLP have all documented the pattern: China, Russia, India, Pakistan, Iraq, Malaysia, Thailand, and the Philippines have received bilateral approval; US-linked and Israel-linked hulls are excluded entirely. Araghchi’s post did not describe a rules-based lane — it left the IRGC as gatekeeper on every individual sailing. Vessel operators have responded with AIS spoofing: hulls falsifying their ownership broadcasts to read “CHINA OWNER” to improve IRGC approval odds. The IRGC statement of 10 April was explicit on where discretion lies: “The initiative for the passage and movement of any vessel is in the hands of the Armed Forces of the Islamic Republic of Iran.” Open is not free.

Mines. The IRGC Navy published a navigational chart on 9 April 2026 formally marking the pre-war international lanes as a minefield danger zone. Maritime analysts with access to the chart have reported that Iran lost track of mines it laid during the opening weeks of the conflict — what was deployed for area denial became physical residue that cannot be guaranteed cleared. Iran’s ten-point peace plan, tabled at the Islamabad talks in April, contains zero mention of mine clearance. The United States decommissioned its four Avenger-class mine countermeasure ships based in Bahrain in September 2025 — there is no dedicated US minesweeping capability in theatre. The “completely open” announcement did not reopen the international lanes. It reopened an IRGC-administered corridor routed around a minefield whose exact location is uncertain.

Clock. The declaration is time-bounded. Araghchi’s post tied the opening explicitly to “the remaining period” of the Israel-Lebanon ceasefire — a ten-day truce that began 16 April at 5pm Eastern and expires 26 April. The truce killed its first civilian in southern Lebanon within twenty-four hours of taking effect; the Lebanese army formally reported Israeli shelling of southern villages on day one. Hezbollah has halted fire but has not endorsed the deal, stating publicly that it keeps “its finger on the trigger.” The US-Iran ceasefire also expires around 26 April. Whatever “completely open” means, it was scoped from the first word to expire in nine days — and the expiry mechanism is already fraying.

This is not a shipping lane. It is a permissioning system administered by a sanctioned entity, routed around uncleared mines, timed to a ceasefire already being violated.

Maersk and Hapag-Lloyd are not holding back out of caution. They are holding back because arithmetic, law, and physics all point the same direction.

The math of “completely open” is unambiguous. Lloyd’s List Intelligence counted 142 vessel transits through the Strait of Hormuz between 1 and 25 March 2026 — a twenty-five-day window that barely exceeds a single pre-war day, during which the strait would typically see between one hundred and one hundred and thirty-five ships cross in each twenty-four-hour period. Divided across the month, March 2026 ran at 5.7 ships per day. Shadow fleet hulls — vessels with obscured ownership, uncertified flags, and irregular insurance — accounted for more than eighty percent of March transits, up from roughly fifteen percent in February. When Araghchi posted on 17 April that the strait was “completely open,” the physical transit number had been running at 94.6% below the pre-war baseline for seven consecutive weeks. The announcement did not change the Lloyd’s count.

March 2026 actual

Pre-war norm

What sits behind those numbers is the backlog, and the backlog is where the arithmetic gets uncomfortable. Reuters reporting, corroborated by Windward AI and CNN Business, counts roughly four hundred loaded oil tankers waiting to exit the Gulf as of mid-April, with another hundred empty tankers waiting to enter. Including container ships, bulkers, and LNG carriers, more than three thousand vessels are present in the Gulf area, of which over eight hundred are oil tankers. At a Very Large Crude Carrier — VLCC, the two-million-barrel standard hull for Middle East-to-Asia crude — the four hundred loaded tankers represent approximately eight hundred million barrels of stranded crude sitting on the water. CNN Business noted on 12 April that even if the strait were to open today at full pre-war capacity, oil flows would not return to normal until July.

The two pipelines that bypass Hormuz entirely have been running at or near maximum for six weeks. Saudi Arabia’s East-West Pipeline — the 1,201-kilometre Petroline from the Abqaiq fields in the Eastern Province to the Red Sea port of Yanbu — was converted to full seven-million-barrel-per-day nameplate capacity on 11 March, after its accompanying natural gas liquids lines were switched to carry crude. The United Arab Emirates’ Abu Dhabi Crude Oil Pipeline — the 360-kilometre ADCOP line from Habshan to the port of Fujairah on the Gulf of Oman — lifted Fujairah loadings from 1.17 million barrels per day in February to 1.62 million in March and has since peaked near 1.9 million. An Iranian drone strike on 9 April knocked roughly seven hundred thousand barrels per day off the Saudi line; Riyadh restored full capacity within three days. Neither pipeline is holding anything back. Together they cover approximately half of the portion of the Hormuz deficit where crude exists and simply cannot ship. They cover zero percent of what has been destroyed upstream. They cover zero percent of Qatar’s LNG.

At the corridor’s current IRGC escort throughput — roughly five to six hulls per day — the eight-hundred-million-barrel stranded backlog takes four to five months to clear. At an optimistic ramped pace of twenty transits per day, the physical ceiling that Lloyd’s and Windward have independently identified, the backlog clears in six to eight weeks. No realistic throughput scenario clears the backlog before the 26 April ceasefire expiry. And no throughput scenario clears the backlog before the Ras Laffan LNG trains that were damaged in Operation Epic Fury return to service in 2027 at the earliest. The arithmetic is physical. The announcement is political. They are running on different clocks.

What the 17 April declaration can do — theoretically, if the sanctions pincer resolves, if insurance is procured, if the IRGC releases specific corridor orders, if the sailing sequence is published, if Hezbollah does not break the ceasefire — is release somewhere between ten and forty million barrels of stranded cargo through the corridor during the nine days before 26 April. That is one to five percent of the visible backlog, and zero percent of the 9.1 million barrels per day of upstream production that is physically offline. The market priced one hundred percent.

The International Energy Agency recorded the largest oil supply disruption in its history during March 2026. Global oil supply fell by 10.1 million barrels per day to 97 million. Export losses through the Strait of Hormuz in March and April exceeded thirteen million barrels per day. The Energy Information Administration projected Middle East production shut-ins of 7.5 million in March rising to 9.1 million in April. The consensus range is now eleven to thirteen million barrels per day of oil offline. None of those numbers is a chokepoint number. They are production numbers, infrastructure numbers, and physical-delivery numbers. The Strait of Hormuz is where the disruption became visible. It is not where the disruption lives.

The Strait of Hormuz is a traffic signal on a road full of destroyed bridges. Eleven to thirteen million barrels per day are offline because upstream production was physically destroyed, bypass infrastructure is already at maximum, Qatari LNG has no pipeline route, and eight hundred million barrels of stranded cargo is clearing at five ships per day. Whether the signal is green, red, or rebranded makes no difference to any of those physical facts. The strait is the symptom. The deficit is the disease.

Roughly nine million of the eleven-to-thirteen is physically destroyed production. Gas-oil separation plants at Khurais and Abqaiq took direct hits in the opening weeks of Operation Epic Fury; the Basra gathering network lost three compression stations to Israeli standoff munitions; the Ras Laffan LNG trains — which liquefy approximately twenty percent of global LNG flows — were struck in a sequence that maritime engineering analyses estimate will require five years to restore. Iran’s retaliatory strikes on Saudi production and on Kuwait’s Mina al-Ahmadi export terminal added further shut-ins. None of this production is paused. It is offline because facilities no longer exist in their prior configuration. The binding constraint on repair is not capital — it is original-equipment-manufacturer turbine backlogs running two to four years, qualified contractors willing to work at war-risk insurance rates, and LNG commissioning timelines that cannot be compressed without multi-year lead-time equipment orders. This is steel and fire brick and rotating machinery. A corridor reopening does not summon a replacement compressor train any faster than it would have arrived the day before.

What flows exist are already moving through every available non-Hormuz route, and those routes are full. Saudi Arabia’s East-West Pipeline is pumping at its seven-million-barrel nameplate — terminal constraints at Yanbu cap practical throughput at three to four-and-a-half million, and every berth is already in rotation. The UAE’s ADCOP line runs near its 1.8-million-barrel peak; Fujairah loadings have ramped as far as the infrastructure permits. Combined, the two lines cover roughly half of the portion of the deficit where crude exists and simply cannot ship through Hormuz. They cover zero percent of Qatari LNG, for which no pipeline alternative exists and for which no pipeline alternative can be built on any timeline relevant to the current decade — the Dolphin pipeline runs onshore Gulf-to-Gulf and cannot bypass the strait, and cross-Peninsula LNG pipelines have never been constructed because liquefaction economics sit at the coast. Twenty percent of global LNG is captive to Hormuz or nothing.

Twenty percent of global LNG flows through Hormuz or nowhere. No overland pipeline alternative for Qatari LNG exists or can be built on any timeline relevant to the current decade. The Dolphin pipeline runs Gulf-to-Gulf onshore and cannot bypass the strait. Cross-Peninsula LNG pipelines have never been constructed. As long as Ras Laffan remains on force majeure — with repair timelines now projected at five years — every month of continued closure compounds the LNG deficit. The toll corridor does not address this. An announcement cannot address this. The captivity is structural.

Non-Middle East substitution is globally zero-sum and mathematically insufficient at scale. United States, Canadian, and Venezuelan exports combined — each constrained by its own independent terminal and pipeline ceiling, as traced in full in GeoNote #5 — contribute approximately 2.8 million barrels per day of theoretically non-Hormuz supply against the eleven-to-thirteen-million-barrel hole. Most of that is not additive at the global level: redirecting existing United States flows to Hormuz-starved buyers creates equivalent deficits in the markets those barrels leave. The shortage relocates. It does not shrink. The genuinely net-new non-OPEC+ capacity outside the Middle East runs closer to one million barrels per day.

The Strait of Hormuz being open does not change any of this. The Strait of Hormuz being shut does not change any of this. The question the 17 April announcement answered — will Iran permit vessels to transit — is the wrong question. The underlying constraint is not a vessel-permission constraint. It is a production and infrastructure constraint. Nine million barrels per day of upstream capacity has been physically destroyed. Twenty percent of global LNG has no route that is not Hormuz. Two bypass pipelines are already at maximum. Eight hundred million barrels of stranded crude clears only at the corridor’s rate-limited escort pace. Global substitution is zero-sum. The eleven-to-thirteen-million-barrel problem persists independent of any declaration Araghchi can make and independent of any corridor architecture the IRGC can administer. The strait is a traffic signal on a road full of destroyed bridges. Turning the signal green does not rebuild the bridges.

Once markets and molecules diverge, the divergence stacks. On 17 April 2026 the divergence stacked into four layers, each priced differently, all of them pointing the same direction until a market could be persuaded to believe otherwise. The four layers now sit on top of each other in a configuration that has existed for seven weeks and has not begun to narrow. What “completely open” did not change is that the paper prices at the top of the stack are lower than the physical prices at the bottom by margins not seen since records began.

Layer 1. Brent crude futures — the paper benchmark most quoted in market commentary — closed at roughly eighty-eight dollars and seventy-three cents per barrel on 17 April after falling 10.7% on the Araghchi announcement. Dated Brent — the physical assessment published by S&P Global and Argus for cargoes of actual North Sea crude scheduled for immediate delivery — was last reliably priced in the $132 to $144 range. On 7 April, Dated Brent reached $144.42 against Brent futures of $109.27 — a thirty-five-dollar same-day gap, wider than any recorded since the benchmark was instituted in the early 1980s. Before 28 February 2026 the gap between paper and physical Brent had run below one dollar per barrel for years. Rystad Energy’s backwardation analysis projects front-month WTI premiums persisting at above fourteen dollars into 2033. The paper benchmark is a forecast of a world with open Hormuz, restored LNG trains, and repaired refineries. The physical benchmark is a price for molecules that exist today.

Layer 2. Physical Dated Brent at $132–$144 is not what an Asian refiner actually pays. To crude priced at the North Sea assessment, add the IRGC transit toll of approximately one dollar per barrel for a two-million-barrel VLCC — a figure that equals the entire 2025 charter cost of the Middle East-to-China tanker route. Add war risk insurance of three to eight dollars per barrel, now standard on any cargo routed through Hormuz or the surrounding Gulf. Add a tanker rate premium of three to six dollars as the TD3C benchmark — the Middle East-to-China VLCC route assessment published by the Baltic Exchange — has nearly tripled. Add two to five dollars for demurrage and vessel waiting during the corridor queue. Add a scarcity premium of five to fifteen dollars as end-users bid up guaranteed cargoes. Asian landed crude is currently running at roughly one hundred and fifty to one hundred and eighty-five dollars per barrel. Brent futures say eighty-eight. This is not a rounding error. This is a measurable wedge between a price the market quotes and a price the market pays.

Layer 3. Refined product prices are where the physical cascade becomes consumer-visible. Asian jet fuel and diesel have settled at above two hundred dollars per barrel for six consecutive weeks. European diesel futures have printed above two hundred after Middle East-bound cargoes were diverted to Asia to service refineries running on depleted crude slates. Singapore middle distillates reached all-time records on 14 April per the IEA’s Oil Market Report. The European Union Energy Commissioner’s assessment to reporters on 15 April was that “this will be a long crisis — energy prices will be higher for a very long time.” Refined product is priced where molecules actually burn. It does not wait for a corridor declaration to clear.

Layer 4. The declaration on 17 April created a fourth mispricing on top of the previous three. The S&P 500 crossed 7,100 for the first time. The Dow rallied approximately nine hundred points intraday. The Nasdaq printed a fresh all-time high. Brent futures fell 10.7%. WTI dropped twelve percent to the low eighties. Heating oil futures fell thirteen percent. Every one of these moves ignored the same-day statements from Donald Trump that the US naval blockade of Iranian ports would remain “in full force” until the nuclear programme is resolved, from Benjamin Netanyahu that Israel had “not yet finished the job” of destroying Hezbollah, and from the Lebanese army that Israeli shelling of southern villages had killed the truce’s first civilian within twenty-four hours of the ceasefire taking effect. The rally was internally inconsistent with the day’s primary-source reporting. It was also internally inconsistent with the other three mispricing layers that have been hardening since late February.

What sits at the top of the stack — equity all-time highs, Brent in the high eighties, the relief narrative — is priced against a world that does not exist. What sits at the bottom — Asian jet fuel above two hundred, LNG on indefinite force majeure, refiners paying physical premiums, eight hundred million barrels of stranded crude waiting for a corridor that can move five ships a day — is priced against the world that does. Paper markets can price narratives indefinitely until they cannot. Physical markets price molecules continuously. The moment the two reconnect — which requires only that the Lebanon ceasefire fail, or that the sanctions pincer clarify, or that the IRGC refuse a single high-profile transit, or that the 26 April expiry arrive — the relief rally unwinds, the futures catch down to the physical, and the four layers snap into one. That is not a hypothetical. That is gravity working on a market that is floating.

For forty years Tehran pursued nuclear capability as the minimum-cost route to strategic immunity. On 17 April 2026, at the same moment markets were celebrating the rebrand of the Strait of Hormuz, Iran’s senior clerical establishment and military command began circulating a different conclusion. A legally codified toll regime on twenty percent of global oil and LNG flows, administered inside sovereign waters by the Islamic Revolutionary Guard Corps, settled in Chinese yuan outside the SWIFT system, is more powerful than a nuclear weapon. It is more profitable. It is more repeatedly exercisable. It is far less provocative. And it is now, in a way nuclear capability never was, backed by Beijing as a structural stakeholder.

The nuclear programme was always means, not end. What Tehran wanted, across four decades and three distinct revolutionary generations, was regime survival combined with regional leverage sufficient to deter intervention. Nuclear weapons were the cheapest available path in the 1980s and 1990s — they delivered deterrence and forced adversaries to negotiate. By 2026, and specifically after six weeks of Operation Epic Fury, the calculation changed. Nuclear facilities are strikable: Fordow and Natanz sit inside identifiable mountain complexes that can be degraded kinetically and have been before. A strait cannot be struck without damaging the striker’s own economy. A toll booth on a shipping lane is infrastructure, not a weapons programme, and the nineteenth-century legal frame of maritime sovereignty provides cover that no enrichment programme can claim under the Nuclear Non-Proliferation Treaty.

The power transfer sits in five specific asymmetries. Nuclear weapons are a single-use deterrent — they generate zero revenue and cannot be exercised without civilisational cost. A chokepoint toll generates approximately one hundred billion dollars per year at pre-war throughput and is paid daily by vessel operators who have no alternative route. Nuclear capability invites pre-emption — Israel has demonstrated repeated willingness to strike Iranian nuclear infrastructure; no coalition has demonstrated willingness to strike a Gulf maritime corridor whose disruption raises global energy prices by forty dollars per barrel. The legal frame of the UN Convention on the Law of the Sea gives Iran a sovereignty claim over the toll regime that it can never have over weapons-grade enrichment. And the yuan-denominated settlement architecture aligns Beijing in as a stakeholder in a way no nuclear capability ever could.

A toll booth on a maritime chokepoint is infrastructure. A nuclear weapons programme is a treaty violation. Iran has found the legal frame that nuclear capability could never provide: the UN Convention on the Law of the Sea gives sovereigns rights over their territorial waters that no non-proliferation treaty clause can override. Tehran does not need to break international law to exercise chokepoint leverage. It needs only to enforce it.

This last asymmetry deserves explicit treatment because it determines whether the toll system is financially sustainable. Iranian oil revenue has been sanctioned out of the dollar system since the first Trump administration. The toll regime, by design, runs on the alternative financial rail Beijing has been building specifically to reduce dependence on SWIFT: yuan settlement through Kunlun Bank on the Cross-Border Interbank Payment System — the Chinese dollar-system alternative known as CIPS. When a shipping company pays the IRGC two million dollars for Hormuz transit, it does so in yuan that never touch a dollar-clearing intermediary. Those yuan accrue to Iran as usable reserves and to China as evidence that its parallel payment rail can carry commercially significant volumes. Beijing thus has both a financial interest in the toll’s survival and a geopolitical interest in defending its legal legitimacy. When China publicly objected on 15 April 2026 that the United States blockade “exacerbates tensions and undermines the already fragile ceasefire agreement,” it was defending an architecture in which it has become a functional partner. No comparable benefit was ever available to Beijing from Iranian nuclear capability.

Point seven of the ten-point peace plan that Tehran brought to the Islamabad talks in April explicitly demands permanent IRGC coordination over Hormuz transit as a formal treaty requirement. This is pre-positioning for a trade. Iran is telegraphing, through a negotiating document, that it is prepared to discuss limits on nuclear enrichment if and only if the final settlement codifies its chokepoint sovereignty. The trade would mirror the Joint Comprehensive Plan of Action of 2015 — enrichment limits in exchange for sanctions relief — with the leverage instrument flipped. In 2015 Iran traded a future breakout capability for immediate economic relief. In 2026 Iran would trade the nuclear programme outright for a permanent, legally formalised revenue stream on twenty percent of global hydrocarbon flows. For Tehran, this is a strictly superior trade.

The architecture is temporally fragile in ways the 17 April announcement did not resolve. The “completely open” declaration was scoped to the duration of the Lebanon ceasefire — a ten-day truce expiring 26 April, agreed between Israel and Lebanon only after President Trump explicitly overruled Prime Minister Netanyahu’s stated preference to continue military operations against Hezbollah. Within twenty-four hours of the truce taking effect, an Israeli drone strike killed the first civilian in southern Lebanon. The Lebanese army reported formal ceasefire violations. Hezbollah confirmed publicly that it was maintaining “a finger on the trigger.” The US-Iran ceasefire expires in the same window. Every element of the 26 April cliff — Netanyahu’s explicit dissent, Hezbollah’s conditional compliance, the nuclear negotiating track’s unresolved status — points at breakdown within days.

Within twenty-four hours of the Lebanon ceasefire taking effect: Israeli drone strike kills first civilian in southern Lebanon — Lebanese army formally reports ceasefire violation. Hezbollah: “keeping its finger on the trigger.” Prime Minister Netanyahu, days before the truce: “we have not yet finished the job” against Hezbollah. The ceasefire that frames the “completely open” declaration was fraying the day it started. The 26 April cliff is not a risk scenario. It is the baseline.

What emerges from the far side of 26 April, in any scenario short of complete US capitulation or complete Iranian nuclear abandonment, is a cold-peace equilibrium. Iran retains the chokepoint architecture; the United States retains the naval blockade and the designation regime. Neither side can force the other to full resolution. A structural Hormuz premium of ten to twenty dollars per barrel becomes baked into long-run Brent. Qatar’s LNG facilities remain on multi-year repair timelines. Global shipping operates under a two-regime architecture that is slower, more expensive, and permanently risk-premium-adjusted. The toll regime establishes a precedent that can be copied: chokepoint monetisation, with its parliamentary legal frame, its yuan settlement rails, and its bilateral-approval discretion, is now a documented blueprint that Bab el-Mandeb operators, Malacca stressors, or Panama under different political conditions can reference. The 17 April announcement did not end the 2026 crisis. It formalised the equilibrium that emerged from it.

Iran has not abandoned its nuclear programme. Iran has discovered that it may no longer need one.

The 17 April declaration is a near-term market event embedded in a multi-year structural deficit. The investment question is not whether Hormuz will transit vessels — it will, in some constrained form, for some nationalities, under IRGC discretion, at a fraction of pre-war throughput. The investment question is what happens on each of three distinct timeframes when the paper market that priced resolution on 17 April confronts a physical market that priced molecules across seven preceding weeks.

The asset class implications follow directly from the reconnection mechanics. Energy producers with upstream capacity outside the Middle East — integrated majors, North American and Norwegian pure-plays, Brazilian deepwater — benefit from a structural Hormuz premium the market has not yet priced into their equity multiples. Tanker operators — particularly the Very Large Crude Carrier fleet servicing Middle East-to-Asia routes — benefit from backwardation, elevated spot rates, and a permanent war-risk insurance differential that has widened tanker spreads by factors not seen in the modern era. Liquefied natural gas export infrastructure in non-Hormuz geographies compounds in value each quarter the Ras Laffan timeline extends. The symmetric short side sits in broad equity indices now trading at all-time highs on narrative relief, long-duration assets whose valuation depends on low discount rates that sustained energy-driven inflation will not permit, and consumer-discretionary exposures vulnerable to persistent refined-product prices above two hundred dollars per barrel. Gold and inflation-linked government debt price the underlying disorder more honestly than either the equity benchmark or the futures curve.

The reconnection of paper and physical oil markets is a matter of when, not whether. The 17 April relief rally priced resolution against a structural 11-to-13-million-barrel-per-day global supply deficit that no corridor announcement can close. The deficit is bound by physical reconstruction timelines — measured in years for upstream production, multi-year for Qatari LNG, and permanent for the chokepoint sovereignty architecture Iran has now institutionalised. Position for a reconnection event before 26 April 2026, and for a structural Hormuz risk premium that persists through 2029 regardless of short-term ceasefire outcomes.

The thesis is wrong if three conditions become true in sequence. The Lebanon ceasefire must extend cleanly past 26 April into a durable multi-month truce with verifiable Israeli withdrawal and explicit Hezbollah endorsement — a scenario with low probability given the Day One civilian fatality, Netanyahu’s stated dissent, and Hezbollah’s “finger on the trigger” posture. The United States must simultaneously lift the Iranian port blockade and Iran must drop the IRGC toll, returning the strait to pre-war Traffic Separation Scheme baseline — an outcome that requires full settlement of the nuclear track, which Trump has stated is the minimum condition for the blockade’s removal. And upstream repair timelines must compress materially despite the binding constraint of original-equipment-manufacturer turbine backlogs — a physical impossibility on anything shorter than a multi-year scale. Any one of the three failing is sufficient to preserve the base case. All three succeeding simultaneously is the residual risk to the thesis. It is not the base case.

The strait was renamed. The deficit was not.